Today we are fortunate to present a guest post written by N. Kundan Kishor (University of Wisconsin-Milwaukee).

Lessons from three decades of long-run forecasts, and what they mean for the AI productivity debate.

Artificial intelligence is expected to reshape the economy, but how much and how fast? Professional forecasters offer one useful benchmark because they are forced to translate broad narratives about technology into specific, quantitative predictions about growth, interest rates, and inflation. The median 10-year productivity forecast in the Survey of Professional Forecasters (SPF) has risen from 1.3% in 2023 to 1.8% in early 2026. Notably, ChatGPT launched in November 2022, yet the first SPF survey after its release (February 2023) saw forecasters lower their productivity outlook to 1.3%. The uptick did not begin until a full year later. This is a meaningful revision, but far below what AI optimists project. The implied equilibrium real interest rate has edged up from about 1.0% to 1.7%. Long-run inflation expectations have barely moved. So who is right: cautious forecasters, or the optimists betting on transformation?

The disagreement reflects a deeper problem: major technological transitions are extraordinarily difficult to identify in real time. Productivity data arrive with long lags, are heavily revised, and struggle to capture the intangible investments, organizational change, and quality improvements associated with new technologies. One way to evaluate whether forecasters are behind the curve today is to study how they performed during the last great productivity debate. The SPF has collected long-run productivity expectations since the early 1990s, and the historical record, spanning the rise and fall of the internet economy, is revealing.

The 1990s: the data hid the revolution

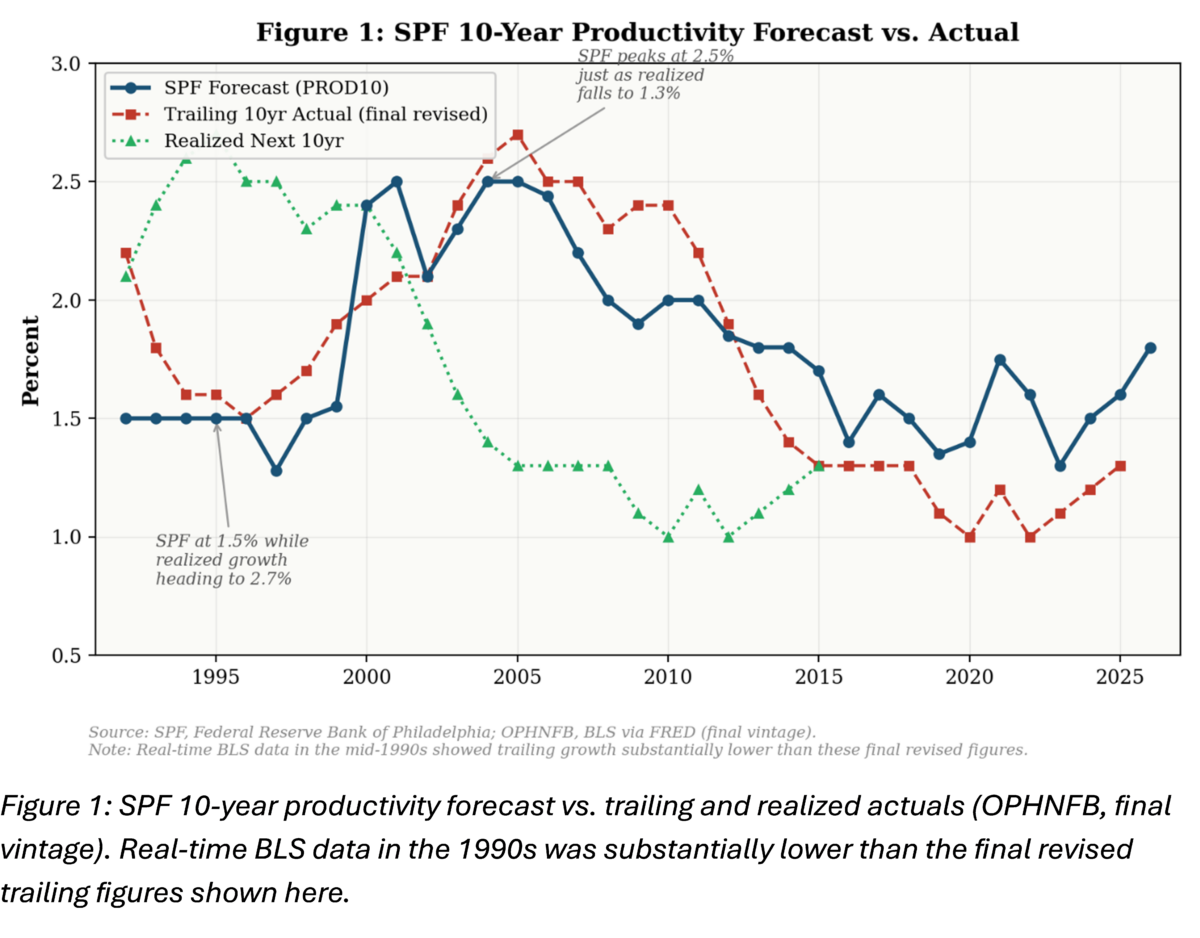

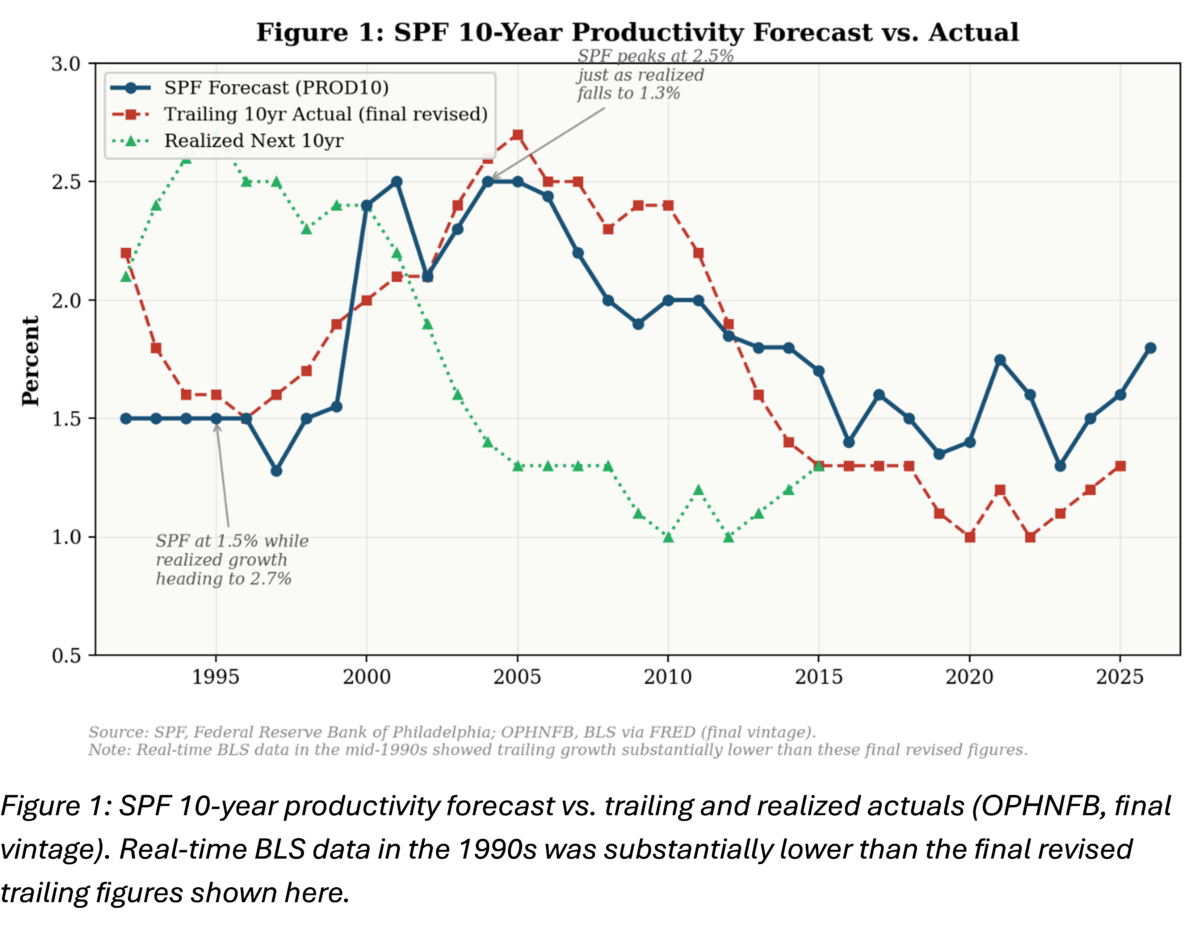

From 1992 through 1998, the SPF held its 10-year productivity forecast at a steady 1.5%. Realized growth over the following decade turned out to be 2.1–2.7%. That looks like a major miss, until you examine what the data actually showed at the time.

In February 1997, the BLS reported that trailing 10-year productivity growth was just 0.7%. The first-release estimate of 1996 growth was 0.8%. After years of revisions (new hours data, the reclassification of software as investment, the 1999 NIPA benchmark), that 0.8% became 2.7% (Jorgenson, Ho, and Stiroh, JEP 2008). The CBO faced the same problem, more than doubling its 10-year projection from 1.15% to 2.7% between 1997 and 2001, once revised data became available. The SPF’s 1.5% was actually optimistic relative to published statistics.

But a deeper pattern persists across the full sample. Figure 1 plots the SPF forecast against final-revised trailing actuals and realized next-10-year outcomes computed from the BLS nonfarm business labor productivity index (FRED series OPHNFB). Forecasters track the recent past closely, and consistently miss turning points. They raised expectations to 2.5% by 2004, just as the boom was ending and realized growth was falling to 1.3%. They lowered them to 1.3% by 2023, just as productivity may be picking up again.

Productivity and the equilibrium real rate

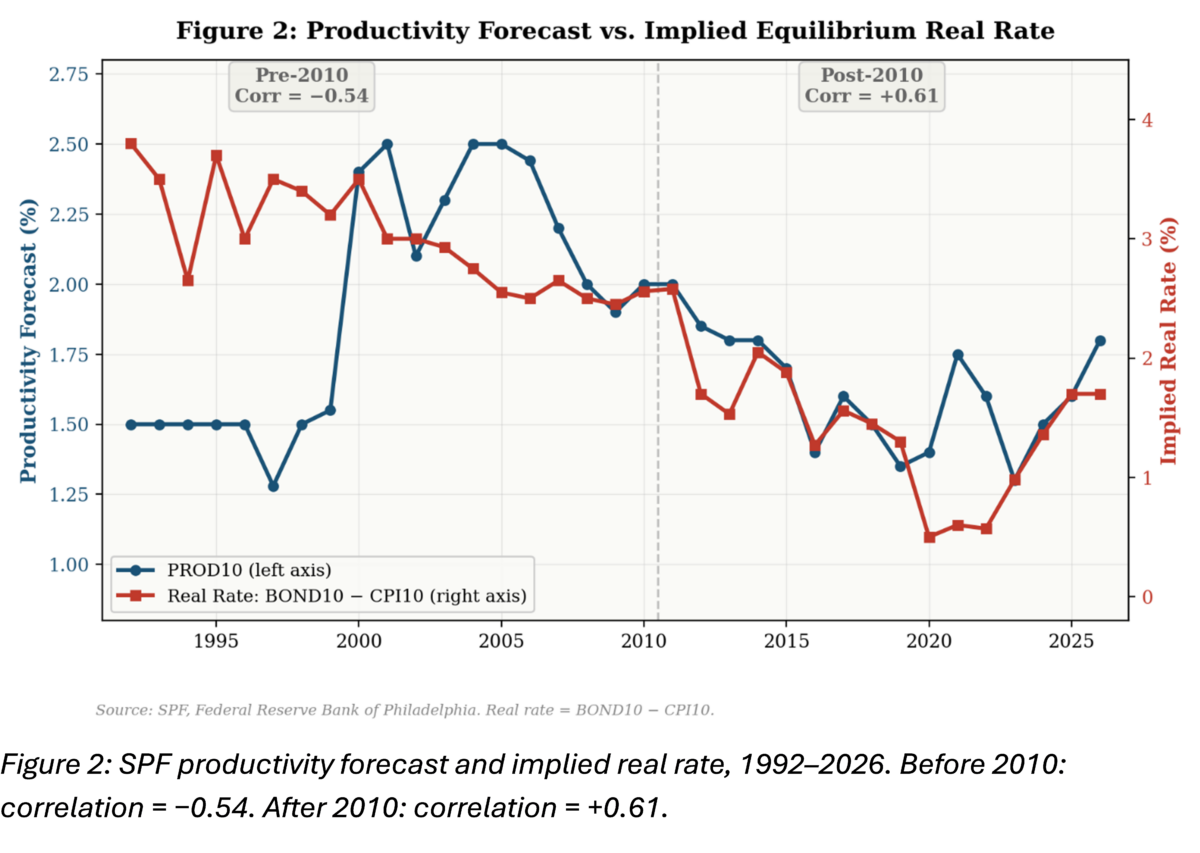

Standard macroeconomic theory is clear: higher trend productivity raises the marginal product of capital and therefore the equilibrium real interest rate. If forecasters use structural models, their productivity and real rate expectations should move together.

For most of the past three decades, they didn’t. Before 2010, the correlation between the SPF’s productivity forecast and its implied real rate (BOND10 minus CPI10) was negative: −0.54. Forecasters who expected higher productivity simultaneously expected lower real rates. This is the wrong sign.

Something shifted after the Great Financial Crisis. From 2011 onward, the correlation turned positive at 0.61. The secular stagnation debate, the prolonged zero lower bound, and an explicit focus on r-star seem to have recalibrated how forecasters connect growth to rates. The recent rise in productivity expectations from 1.3% to 1.8% has been accompanied by a real rate increase from 1.0% to 1.7%, modest but in the theoretically correct direction.

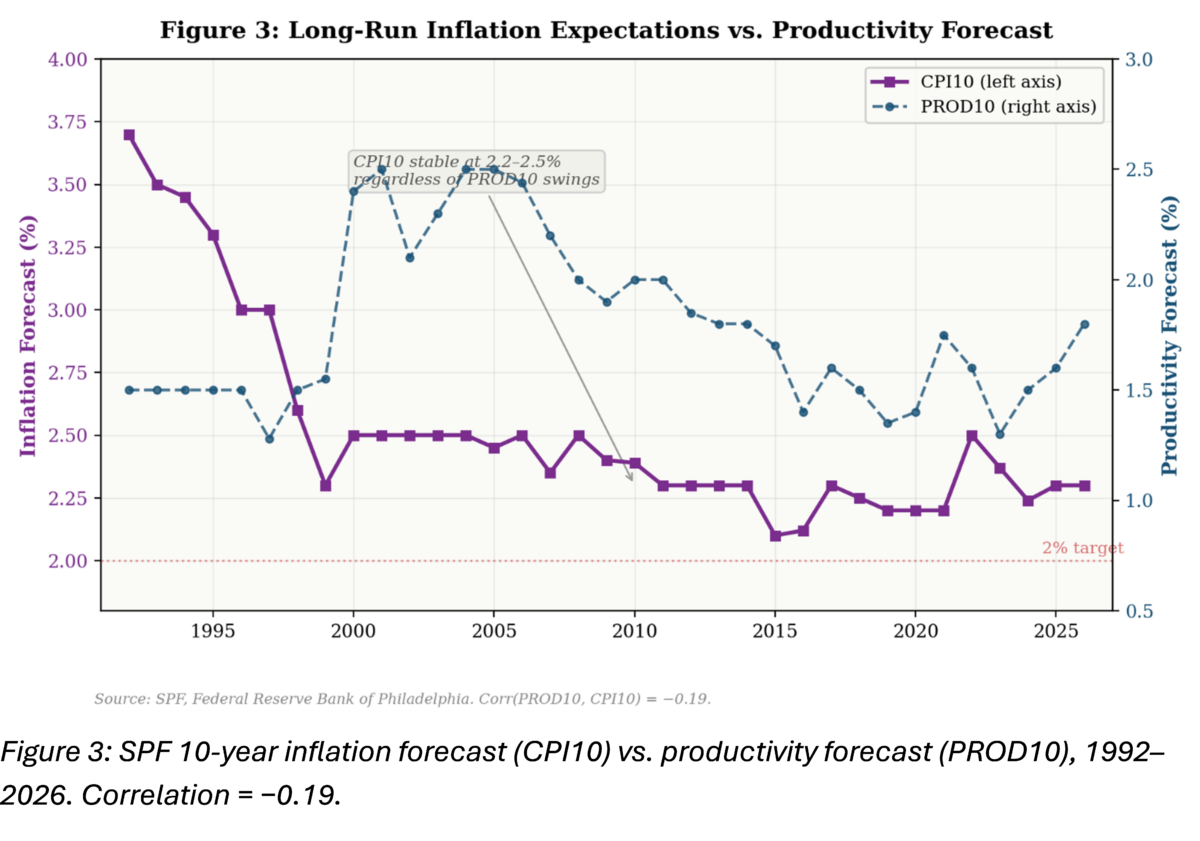

Productivity and long-run inflation: remarkable anchoring

If productivity matters for real rates, does it also matter for long-run inflation expectations? Theory offers competing predictions. Higher productivity could reduce inflation through lower unit labor costs, or it could be neutral if monetary policy adjusts to maintain its target.

The SPF data give a definitive answer: long-run inflation expectations are essentially invariant to the productivity outlook. The correlation between PROD10 and CPI10 is just −0.19, effectively zero.

Figure 3 makes the point visually. While the productivity forecast has swung between 1.3% and 2.5% over three decades, the inflation forecast has been remarkably stable at 2.2–2.5% since the mid-1990s. The early-1990s disinflation (CPI10 falling from 3.7% to about 2.5%) was a one-time adjustment as inflation targeting gained credibility. Since then, even the 2022 inflation shock barely moved CPI10. It ticked up to 2.5% and has already reverted to 2.3%.

This is arguably the strongest evidence of inflation expectations anchoring in the SPF data. Forecasters treat the Fed’s long-run target as fully credible and view productivity as neutral for long-run inflation. Whatever AI does to the real economy, the SPF consensus is that it won’t change where inflation settles.

What this means for the AI moment

The parallels to the 1990s are hard to miss. Massive technology investment, dramatic early-adopter gains, official statistics that remain modest. Just as the IT revolution was well underway by 1995 but the SPF did not budge until 2000, the AI moment has so far produced a delayed and cautious response. If AI’s impact arrives first in hard-to-measure services, the data may lag even more than during the IT revolution.

But the 1990s also teach caution about the optimists. The “new economy” narrative ran years ahead of the data that eventually validated it, and not all of those projections survived contact with reality.

The SPF data reveal a forecasting consensus with a specific structure: cautious on productivity (1.8%), modestly higher real rates (1.7%), and fully anchored inflation (2.3%). If AI delivers even half of what its proponents expect, the productivity and real rate numbers are likely too low, and the policy implications are significant. If it doesn’t, the current consensus will look prescient.

The lesson from three decades of productivity forecasting is not that professional forecasters are poor at their jobs. It is that structural breaks are genuinely hard to see in real time. The question isn’t whether AI will transform the economy. It’s whether the data will let us see it when it does.

Data: Survey of Professional Forecasters, Federal Reserve Bank of Philadelphia; Nonfarm Business Sector Labor Productivity (OPHNFB), Bureau of Labor Statistics via FRED.

Real-time data revisions discussed in Jorgenson, Ho, and Stiroh (2008), “A Retrospective Look at the U.S. Productivity Growth Resurgence,” Journal of Economic Perspectives, 22(1), 3–24.

This post post written by N. Kundan Kishor.

By

By