Yves here. Michael Hudson and Radhika Desai discuss many of the long-operating forces that have been eating away at the foundations of the American economy, from its super-sized military to neoliberalism and financialization, now exhibiting many late-stage pathologies, from asset speculation to extreme wealth concentration. And as bad as those trends have been, Trump has succeeded in making them worse.

Radhika Desai:

Hello and welcome to the 80th Geopolitical Economy Hour, the socialist and anti-imperialist conversation that illuminates the fast-changing political economy and geopolitical economy of our time. I’m Radhika Desai, and you’re watching Radhika Desai, Geopolitical Economist. Today’s Geopolitical Economy Hour is our regular one with Michael Hudson, which we do every fortnight. Welcome, Michael.

Michael Hudson:

Glad to be back!

Radhika Desai:

Great, Michael. Today we have decided to talk about the US economy under Trump. Now, of course, Trump is doing everything in his power to suck the oxygen out of the story about the economy. That includes continuing to escalate wars and all sorts of diplomatic and other shenanigans that he is constantly involved in, berating leaders of other countries and generally trying to make a big spectacle of himself. This is what he has done with his attack on Iran most recently, with all these crazy bets that he is making, like charging 20% to all the ships that pass through, and in return he is going to be the guardian of the Strait of Hormuz. How can he charge 20% to anyone unless Iran lets these ships through? And how can he be the guardian of the Strait of Hormuz? Iran is completely in charge of it. Anyway, all of these shenanigans are designed to distract attention from the biggest story, the condition of the US economy. Notwithstanding his unhinged and genocidal antics, the topic of the US economy simply will not go away. The world is settling down to summer before the midterm elections, and assessments of the US economy are proliferating. That is what we are going to talk about today, because the US voter votes on her economic condition, and her economic condition is not looking good at all. Michael, what are the headlines from your point of view?

Michael Hudson:

Well, the headline is really that the US economy is all about Donald Trump right now. The main thing, as you have just pointed out, is the war with Iran that he is escalating. Instead of rolling things back, he is bombing Iran. Iran has taken a response that is irreversible. It has closed down trade not only in the Strait of Hormuz but also in the Red Sea, with the Yemenis’ support, and it is bombing Bahrain’s port. It is absolutely certain that there is going to be a shutdown in the oil trade, and that is going to affect the entire world economy and push it into what I think is going to be as serious a depression as the 1930s. That is the US economy. What we can do is spell out how this is happening, because what is the US economy? It has been a huge expansion of financial wealth without any real expansion in living standards, real wages, or prosperity for most of the population. All of this financial wealth has been based on credit. Companies are not making more profits. The whole leadership of the stock market has been the seven AI companies linked to computers. AI is not making a profit; it is all speculation that we are going to expand and that there is going to be a huge market because everybody is going to use AI. But all of this market is dependent on computer chips that run on energy. We are going to see energy prices go way up, and that means electricity prices are going to go up. I want to briefly explain why the oil war is so important when we talk about the economy.

Radhika Desai:

Michael, before you continue, let me just share this because you are referring in particular to the Financial Times article where Adam Tooze is saying that we are moving from essentially the Treasury-based dollar to the profit-based dollar. At one level, this is what I have been saying all along: it is not the buying of US Treasuries that has been keeping up the US dollar for the last quarter century or more; it is the expectation of profit that has been created when the United States has been blowing up asset bubbles—whether it is the dot-com bubble, the housing and credit bubbles, or now the everything bubble. The only problem with Tooze’s article is that he talks about the profits as though they have been realized, whereas it is the expectation of profits, and as we have seen, every time the bubble bursts… so sorry to interrupt, but please continue.

Michael Hudson:

I want to explain just how that works. My whole premise in Super Imperialism is that after the United States went off the gold standard in 1971, all of this military spending, which is the major cause of the balance of payments deficit, ended up in foreign countries. The recipients took the dollars, turned them over to the central banks, and the central banks bought Treasury bonds and Treasury securities. What has happened in the last few years is that banks have stopped buying Treasury securities. The growth in international reserves has taken the form primarily of buying gold, not Treasury securities, and yet the US dollar remains strong. What has happened is that the private sector that has been receiving these dollars has not been turning them over to the government to recycle to the US as Treasuries, as you and I have been talking about. They have spent them into the US stock market. What has that done? It has inflated prices and ridden on the wave of the Federal Reserve supporting the banking system and creating huge asset price inflation, starting with the zero-interest-rate policy that Obama began. What has been creating all this financial wealth, making trillions of dollars for financial investors, has not been profits. It has been the ability to borrow at a low interest rate, including low interest rates in Japan, to buy US securities, bid up the prices of stocks, and create a huge credit overhead. So it is not a profit bubble; it is a Ponzi-scheme capital-gains bubble. It is a credit-creation bubble.

The problem is what happens when there aren’t the profits to support the stock buyback programs and the dividend payouts that have enabled borrowers to carry the debts they have taken on to bid up the stocks. If the credit begins to be rolled back here, and two weeks ago we talked about how Warsh and Bessent want to roll back the Federal Reserve’s balance sheet, they want to begin selling the Federal Reserve bonds that they have been buying in recent years to help liquefy the economy. The economy is going to be made much less liquid, and all of a sudden it is like a Ponzi scheme. A Ponzi scheme requires more and more people buying into it to provide the revenue to pay off investors. If interest rates go up, there is no more recycling of all this money into the stock market to help support things, and there is going to be a huge write-down. When that happens, stocks begin to fall. With higher energy prices, higher food prices, and higher costs of doing business, companies will go out of business. The Financial Times and main business sites have been saying the real problem is private equity. They have borrowed money from the banking system to buy companies, and now some of these companies are going to be running losses and closing down operations because it is not profitable to operate with high oil prices, high energy prices, and high electricity prices. Once they close down operations, they will not be able to pay the debts they have taken on, creating the same snowball effect that people expected in 2008–2009, when Obama decided on a bailout of the banks and decades of asset-price inflation to keep the bubble going and save the banking system. We are talking about the dynamics set in motion by the oil war, the rise in energy prices, and the AI demands for electricity that cannot be met because there is no electricity supply. All of this hopium has evaporated, and the result is going to be the serious depression we have been talking about all along. Yet the stock market idles along as if everything is all right. Our point is that these changes are irreversible. You cannot reverse a debt-inflated economy without wiping out the debts. How does that happen? Companies go bankrupt. There is not going to be a Brady Plan for the American economy. It is going to be companies going broke, and there will be a capital flight out of the dollar, not into the dollar. The whole world balance is being thrown out of kilter in a way that, unlike 2009, there is no monetary solution to a problem of actual physical supply of energy, electricity, oil, and chemicals not being available. This is the grand interruption that we are going to be talking about.

Radhika Desai:

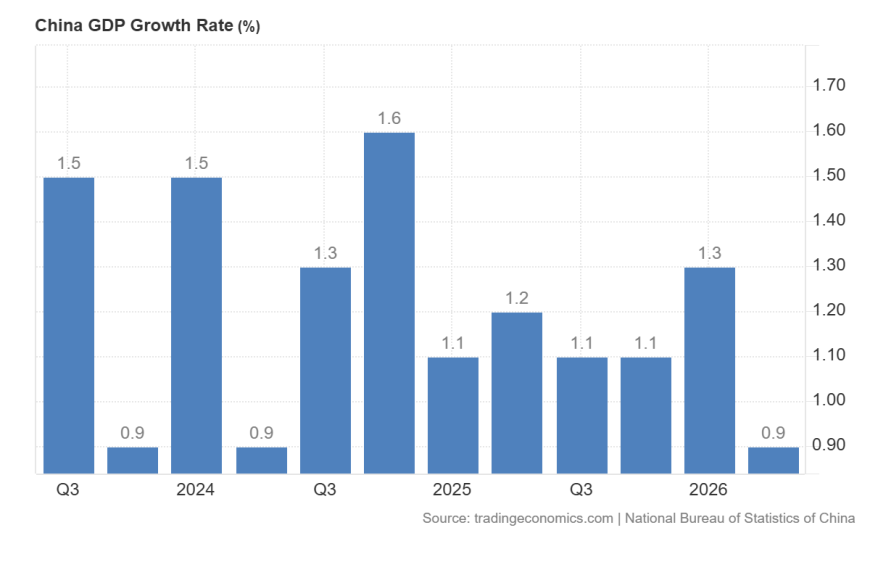

Michael, there are so many interesting points you are making, and you are quite right, we have been essentially warning about this. I started the Geopolitical Economy Hour back in early 2023, and we have been doing shows ever since. You have been one of my most regular guests, and we have been talking about this. Let me break down what you are saying. First of all, I would say that serious though the crisis is going to be, it is not going to be as serious as the Great Depression. The reason has nothing to do with anything good that Trump might be doing; it has everything to do with the fact that, unlike in the Great Depression, today we have another center of world growth other than the capitalist economies: China. China is already exerting an enormously stabilizing effect on the world economy. Let me give you one example. People are remarking that the price of oil has not gone up as much as had been feared, even in the worst moments of the crisis. The main reason is that China has done two things that have kept oil prices lower than they might otherwise be. First, it has accelerated its transition away from fossil fuels toward renewables, it is far in advance of most countries. Second, to the extent that it still relies on fossil fuels, it has created an enormous reserve of oil.

Second, the argument you are making, that all this trading essentially since the 1990s, if not earlier, has meant the United States opened a giant casino, a Ponzi scheme, relies on the rest of the world bringing money in, but every instance of money coming in has proved to be a bubble that burst. To keep the bubble going, the United States has relied on low interest rates. In addition to my writing on geopolitical economy and the article you and I co-authored on the dollar-creditocracy, I have also written two shorter pieces analyzing Powell’s speeches in 2023 and 2024 justifying monetary policy. I argued that Powell was not able to increase interest rates to the extent necessary to quell inflation if increases in interest rates were the only method. Of course it is not, but that is the only way the Federal Reserve does it. The result has been interesting. If you look at a chart going back to 1955, the blue line shows the federal funds effective rate, and the red line shows the inflation rate. Through most of the Federal Reserve’s career, except for the 1970s, inflation has remained below the federal funds rate. But starting in 2000, you see frequent instances where the federal funds rate has been below the rate of inflation, creating negative real interest rates, the easy-money policy on which the bubbles have been based. In the early 1980s, Paul Volcker allowed interest rates to go as high as nearly 20% to deal with inflation. That option is no longer available to the Federal Reserve. It must appear to deal with inflation, but even higher interest rates remain below the level of inflation. So in this century, the Federal Reserve has been very tolerant of inflation, eating into the dollar’s value. You said earlier that the dollar is high, but actually it may be high compared to what it was until recently. The overall trend of the dollar has been to go down under the Trump administration. Since Trump took power in January 2025, the trend is downwards. Yes, recently it has gone up a bit, but the buzz in the financial press is that considering the Iran conflict has been raging, and normally you expect the dollar to go up during any international crisis, the dollar has gone up by much less than you would think. A chart from The Economist plotting the dollar under Biden, Obama’s second term, and Trump’s first and second terms shows that while the dollar rose under Biden and was more or less indifferent under Obama, under Trump in both cases the dollar has declined. Trump promised he wanted the dollar to be the world’s currency, but everything he has done endangers the dollar’s role. One of the main reasons the dollar system is endangered is that all the money coming into the dollar system from Japan, Western Europe, and the Gulf countries has been what is keeping it up. All three are going to find other uses for their money. All are facing economic crisis; in the case of the Gulf countries, a profound security crisis; in the case of Europe, a security crisis of their own devising. So the money coming from those three main sources is going to go away, creating a big problem.

Michael Hudson:

The key is what all this money coming into the US economy has been spent on. As you said, it has not been spent on industrialization or increasing the means of production, the kind of things China is spending its credit on. It has been spent onx§ stocks and bonds. I wish your chart had charted the relevant price inflation, which is asset-price inflation: how much stocks, bonds, and real estate have gone up. Those are the prices the Federal Reserve is concerned about. It does not care about consumer prices because monetary policy has almost zero effect on consumer prices. The Federal Reserve and banks do not lend primarily to wage earners to spend on goods and services, except through credit cards, student loans, and personal debts. Basically, the Federal Reserve creates credit to buy assets, not goods and services. That is what it is all about. When you buy assets, it is a financial transaction, not part of the consumption and production economy.

Radhika Desai:

Exactly, but that chart shows exactly that. Of course it does not show asset prices. Can I clarify? The Federal Reserve never says it is trying to keep asset inflation down; it never says anything about asset-price inflation. It always makes its pronouncements based on consumer inflation and justifies its monetary policies using consumer inflation. It relies on the idea that inflation is always a monetary phenomenon, so easy money policies gives rise to inflation and tight money policies quells it. But even though consumer price inflation has been rising, the Fed has no cards, to put it in Trumpian words, to deal with it, because secretly its monetary policy has always been about inflating asset prices. That has been the chief mechanism through which the casino has operated. So, we are in agreement.

Can we deal with the issue of inflation? Trump agreed he was going to kill inflation. His economy was going to revive, inflation was going to expire, the price of eggs was going to go down. In reality, inflation has remained sticky, further heightened by his tariffs, and threatening to keep going up because Trump refuses to end the war in Iran because he refuses to face the inevitable, that he has lost the war against Iran. The only reason inflation is not even higher is that US workers, despite heroic struggles, have failed to increase wages in line with inflation. Their real wages have declined, so they have not contributed to inflation, but they are suffering from it. Trump has failed awfully on inflation.

Michael Hudson:

The war in Iran and OPEC trade is not a monetary phenomenon. Milton Friedman and the Chicago School promoted junk economics that Federal Reserve money creation creates inflation. We are talking about reality: the cost of production, the cost of imported oil, the break in the chain of payment, and the shortage of oil. That is what is causing inflation, which is why Trump is doing his shakedown of OPEC, saying they have to send money into our economy. Regarding what you said about the dollar not rising, this is very important. Trump thought that if the dollar goes down, it would make US industry more competitive, just like we tell Global South countries to break up unions, reduce labor costs, and cause unemployment to become competitive. This is more junk economics. The dollar going down is not really going to make American industry more competitive because industry has moved out. What it does mean is that if the dollar is going down, countries are not going to make what is implicit in the chart you drew. Countries have been making not only highunder the zero-interest-rate policy, but by investing in stocks, bonds, and asset prices. That is the new kind of arbitrage: It’s not by buying borrowing in Japan for under 1% and buying U.S. bonds yielding 4 or 5% or up to junk bonds. It’s by borrowing in Japan for under 1% and buying stocks yielding dividends, using profits for stock buybacks to increase prices, and buying bonds that go up in price as interest rates go down. It is speculation. That is what the whole economy has been based on. But asset-price inflation based on a Ponzi scheme without underlying investment, employment, or productive capacity can only last so long. All of a sudden we are seeing the result of America not doing what China is doing and what America did in the 19th and early 20th centuries to get rich, actually investing in means of production. How long can you sell stocks and bonds in an economy that is shrinking? International reserves have not been buying dollars with the influx of foreign military spending pouring into the world economy. They have been buying gold, or the private sector has been investing more in China, not just Chinese stocks, but moving physical plant, like Volkswagen and German industry fleeing the West because NATO is deindustrializing Europe. That is the big news.

Radhika Desai:

Let me show this chart of inflation. It goes back to May 2016. You can see the big increase due to COVID, then it came down in 2023 or thereabouts, and then it remained relatively elevated. Under Trump, the last date here is May 2026, and there has been an enormous spike. Trump has failed on inflation. He also promised the American economy would boom like never before. Let us look at ordinary GDP figures going back to 1966. GDP growth rates before 1980 were considerably higher on the whole than since. But the GDP growth rates for 2025 and 2026, just an estimate for now, are considerably lower than even the lower rates of recent years. Trump has not delivered on growth either.

Michael Hudson:

I want to remind viewers that not only has GDP not increased, but the component of GDP is not industrial growth. Most of this so-called GDP growth is not product at all; it is interest rates and economic rents. Late fees on credit cards are called providing a financial service and counted as a product. Another element of GDP, when the government asks homeowners what they would have to pay in rent, as asset prices go up and rents go up, they say they would have to pay more, so that increase is counted as GDP. None of this is a product, but it is counted because of the myth that there is no such thing as unearned income, no such thing as economic rent that adds to price without value. When a credit card bank imposes a late fee, it does not produce a product. When the 1% make more interest and capital gains and landlords make more money on real estate, that is not a product, but it is all considered GDP. That is the fake junk economics that has shaped the concept of gross national product.

Radhika Desai:

Here is the practical demonstration. Under neoliberalism, since the 1980s, the era of deregulation, financialization, and deindustrialization, manufacturing employment remained elevated until 1980, then began a secular decline, particularly steeply in the new century. From 2010 onward, it stabilized a bit. Since 2021, after the COVID dip and recovery, it has been declining. Here is Trump’s inauguration in January 2025. It has continued declining. All the tariff shenanigans have achieved nothing. He promised to create more manufacturing jobs, but job gains have been confined to healthcare and education. More than 100,000–113,000 manufacturing jobs have been lost. Reasons cited include higher labor costs (in part due to inflation, though workers have failed to keep up), a shortage of skilled workers due to Trump’s clampdown on immigration, and continued policy uncertainty, the opposite of what any investor needs. There is absolutely no policy certainty with Trump. The unemployment rate is low, but it only counts those actively seeking work; it does not count discouraged workers who have stopped looking for work. The labor force participation rate peaked around 2000 at about 67% and has declined to about 61% today. Since Trump’s inauguration, it has declined even more. You cannot blame people, given the complete joke he has made of serious economic policy, that it has discouraged investment and job creation of any serious sort.

Michael Hudson:

These points about labor are very important. It is not only skilled labor; it is also manual labor. The New York Times had a good article that the job everybody really wants is working for the subway as a clear. A cleaner can make $200,000 a year; the average plumber makes over $100,000, more than college graduates who become social workers, psychologists or part-time adjunct professors. Last year, when Trump tried to negotiate with Asian and European countries about investing in America, Korea, Japan, and Taiwan said they could not find skilled labor in America to build factories because the education system has not been geared to that. You cannot go to school to learn industrial work without taking on student loans and heading into bankruptcy. Regarding labor force participation, most of the decline is because Americans are getting older, but people over 70 cannot retire; they have to find some job, maybe at McDonald’s, because they cannot live on social security and pensions unless they joined a union, but of course unionization has gone way down. What the chart does not indicate is off-the-books labor, immigrants working in healthcare, home care, maids, or agriculture. In the last two months, the biggest jumps in employment have been in healthcare, which is for all the immigrants that have been deported. Americans now have to pay for that, so the actual cost of labor has gone way up because you cannot cheat Americans like you can cheat immigrants by seizing their passports and threatening deportation. This whole crooked employment system is broken up, increasing the labor squeeze. We are having a perfect storm of everything that can go wrong. Trump has made a list of how to destroy the American economy and end the American century and he has done it.

Radhika Desai:

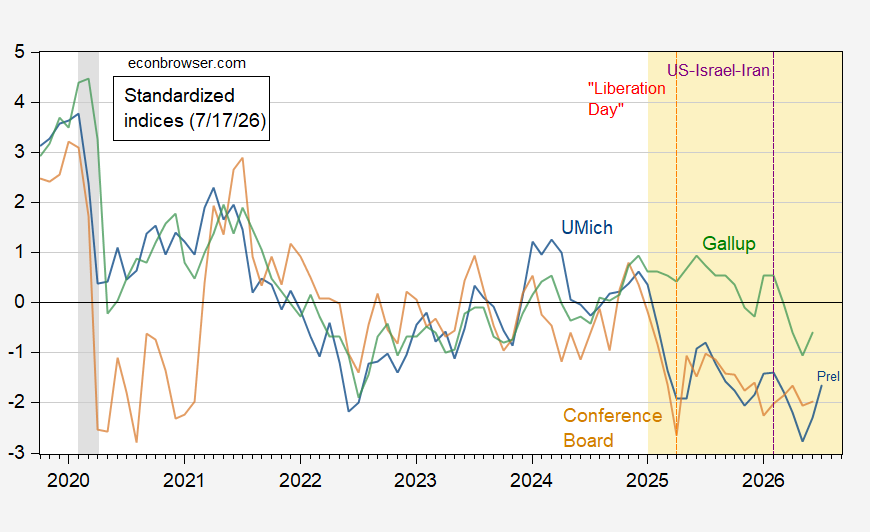

Considering the number of times he says he is the greatest president ever, forget Washington, Lincoln, Jefferson, Roosevelt, he is the greatest ever. The sheer scale of the delusion is amazing. Let us come to the closing part. All the stuff we have shown has been doing badly, but one thing has been doing excellently: the stock market. Here is a chart of the S&P and NASDAQ since 2010, precisely the time when the US economy entered its doldrums, labor force participation went down, growth is down, manufacturing is down, deindustrialization is rampant. What is going up? The stock market. You would think the stock market would reflect productive investment, but it has taken leave of the productive economy. It is like a balloon a child has lost hold of, no longer connected to anything, simply going up and up. At the same time, consumer sentiment has gone down. Under Trump, it has declined more or less consistently. Here is the reason, everyone is talking about the K-shaped economy. An article from The Guardian says the top 10% account for more than half of consumer spending, while the other 90% account for the other half. Airlines are adding more business class seats as the wealthy clamor for them, but Spirit, the low-priced airline, has gone belly-up. Private jet and fancy yacht sales have soared, even as the Federal Reserve says more Americans are going hungry. McDonald’s CEO complained of a two-tier economy, with sales to lower-income Americans declining even as McDonald’s added premium products like the Big Arch Burger, costing $7.50 to $13. Wealthy Americans fly to Greece and African safaris; average Americans are squeezed by $4.26-a-gallon gas, cutting back on travel and piling on debt. US consumers have shelled out $52 billion extra for gas due to price increases. As with Trump’s tariffs, soaring gas prices have squeezed non-rich Americans more than rich ones, the bottom quarter, earning $40,000 a year, spend about 4% of their income on gas, while the top fourth spend less than 1%. This is just a tiny picture of the horrific K-shaped economy.

Michael Hudson:

The K-shaped economy is what we really should be talking about. You mentioned the stock market going up. 85% of US stocks are owned by about 10% of the population.

Radhika Desai:

Michael, have I got a chart for you! The wealthiest 1% have seen far greater gains in the past 25 years, from $10 trillion to over $50 trillion, while the bottom 50% have gone from nothing to nothing.

Michael Hudson:

That is exactly the point. All of this attraction of the American economy to foreign investors, recycling military spending dollars back into the United States, is part of a dynamic that benefits the 1%, not the bottom 90%. The American attraction is not for the productive economy, not for employment or consumption, but for the bubble economy. That’s it, the bubble is the attraction. Does Trump have anything at all? I do not think he is trying to destroy the economy; he just believes the junk economics that is destroying it. He is a sucker for what they teach in economics courses. His solution is to establish choke points, monopolize what we can and hold it over foreign countries. If we can exclude Venezuela, Iran, and Russia from the oil trade, we can control it and charge whatever we want. If we can control the AI revolution, nobody will be able to use computers without paying enormous rents to the magnificent seven companies. The idea is that America can become a monopoly economy, not industrial capitalism, but monopoly capitalism of a financial form. That is behind the K-shaped economy. The whole idea is that if you can focus on the economy of wealth, which is not about production, consumer prices, GDP, or output, but about financial wealth. That is what people look at. How much is your home worth? How much is your real estate worth? How much are your stocks, bonds, and retirement account worth? That is what the measure of wealth is, Instead of: How are you living? What are your living standards? All of that, without people realizing that there has been a bait-and-switch. People think the economy doing good means they are doing good, but it is the 1% and 10% doing good.

Radhika Desai:

What you are calling the monopoly economy, the rentier economy, the economy of unearned incomes, that is what is increasing in size. People always claim the United States is still richer, but the gap between average income (around $80,000) and median income (closer to $40,000–$50,000) is enormous. The average is stretched up by astronomical incomes of the likes of Elon Musk and Jeff Bezos. At the end of the day, theirs is the economy of takers, but the economy of takers cannot exist without the economy of makers, and the economy of makers is shrinking. That is one reason the crash is coming. US state policy is essentially to try to be takers from everybody, working people in the United States and producers all over the world. But more and more of the rest of the world is going to refuse to allow them to take. By shrinking the economy of makers within the United States, they have endangered the economy of takers. When the big crash comes, the dollar system, the principal means through which the United States siphons off value from the rest of the world, will also crash. We started this conversation talking about the state of the economy and how it will affect the midterm elections. There is no doubt in my mind that, given the dire state of the economy for ordinary people, there is going to be a big upset for Trump. He is going to lose control of Congress, who he loses to remains a mystery, and perhaps we can do another show on that. But ordinary people, including Trump’s own MAGA base, are losing faith in him. The New York Times approval rating chart from Inauguration Day shows that since March, the disapproval rating has climbed to 58% while approval has declined to 39%. This is why Trump, in desperation, started wars in Venezuela, Iran, and God knows where next. None of these wars have turned around his approval ratings. He broke every promise he gave to win the election, he promised ordinary Americans the moon, and instead they are being thrown into a deep pit. This is bound to have an effect. While I have never particularly admired American democracy, if people do reject Trump, it will revive American democracy to some extent.

Michael Hudson:

I would not want to end on a negative note. Let us look at the good backwash of the things Trump has done. You pointed out the Democratic Party is dead, there is no alternative to Trump’s policies from the Democrats. They are all in favor of the war in Iran, the war against Russia, NATO, and the stock market because they are funded by the same people. The result of Trump’s aggressive policies, and the Democrats’ too, is that America is isolating itself from the whole rest of the world. By trying to isolate other countries with sanctions, it has ended up sanctioning the American economy itself and ending the American-centered world order. Let us give Trump credit for that, and the Democrats too for going along with it.

Radhika Desai:

On that ironic note, Michael, I think we should bring our show to an end. Thanks again for coming here. We will meet again in a couple of weeks and talk about something else equally interesting and important. Meanwhile, thank you very much. Thanks to our audience. I hope you liked what you heard. If you did, please like, subscribe to the channel, share widely, donate if you can, and until next time. I will see you later. Bye-bye.

By

By