Consider Germany over the last four years:

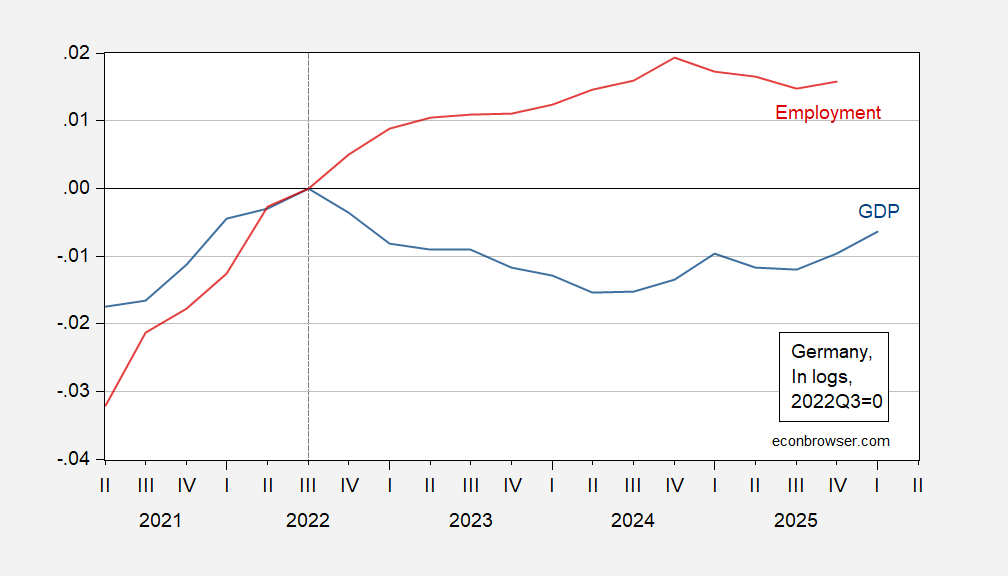

Figure 1: German GDP (blue), and employment (red), both in logs, 2022Q3=0. Source: OECD via FRED, and author’s calculations.

For the period that GDP was declining, employment was rising, up to 2024Q4. As a consequence, neither the German Council of Economic Experts, nor (private sector firm) ECRI or nonprofit Conference Board have declared a German recession.

Interestingly, there is no active prediction market on Kalshi for a German recession. That’s because the rules define two consecutive quarters of negative GDP growth as a recession, so the market is labeled as “determined”. (In contrast, for the US, Polymarket relies on either the 2 quarter rule or a NBER determination).

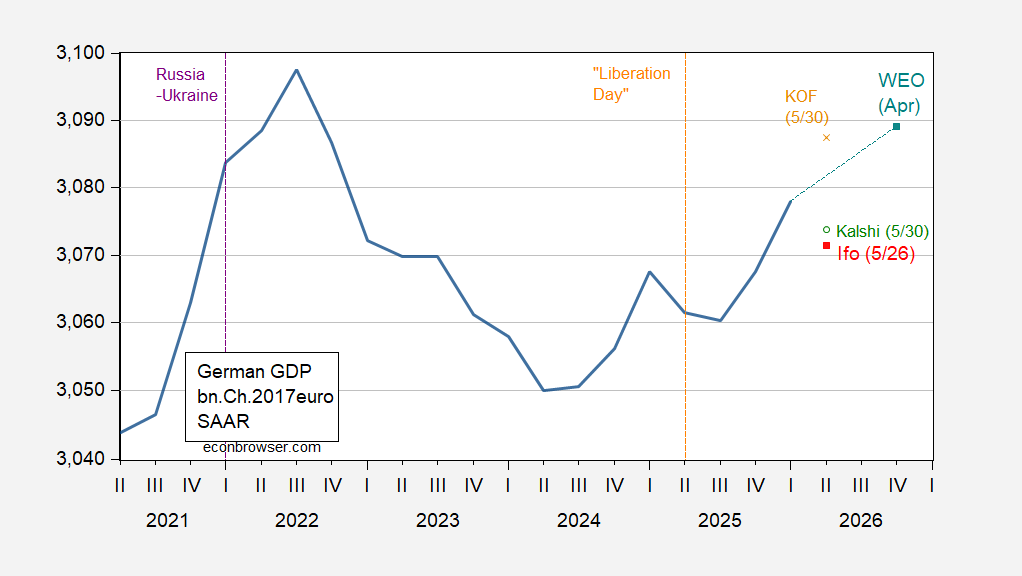

What’re prospects for Q2? Here’s a picture of GDP incorporating the latest Ifo forecast of 5/26, and the IMF’s WEO baseline projection of April.

Figure 2: German GDP (blue), Ifo nowcast of 5/26 (red square), KOF nowcast of 5/30 (tan x), Kalshi betting as of 5/30 (green circle), and April 2026 WEO baseline (teal square), all in bn.Ch.2017Eur SAAR. Source: OECD via FRED, Ifo, Kalshi, KOF, IMF, and author’s calculations.

The Ifo number is of a bean counting exercise, as is the KOF (Konjunkturforschungsstelle/Swiss Economic Institute) Nowcasting Lab estimate. The Kalshi odds are a mix of differently conditioned bets, while the WEO projection conditions on very specific assumptions (as laid out in the WEO, especially regarding oil and natural gas prices).

By

By